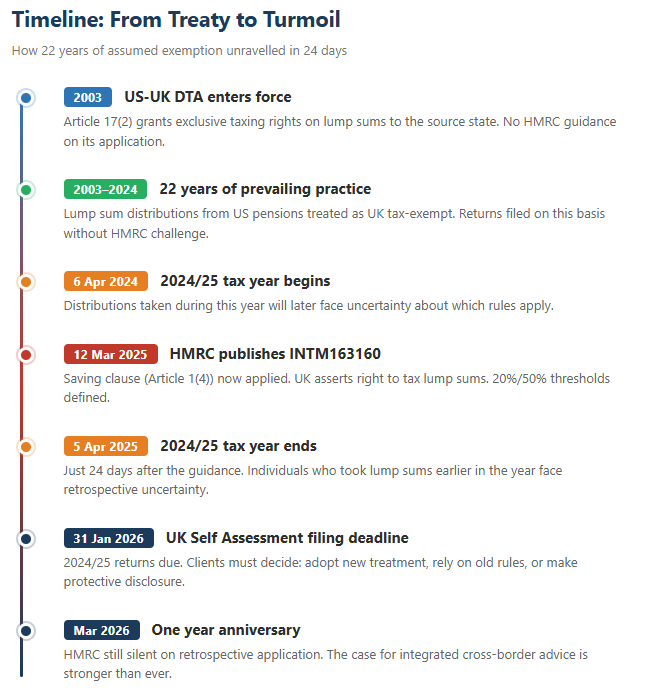

The HMRC changed US Pension taxes on the 12 March 2025. Many advisers and expats in the US/UK community read the HMRC published statement in its International Manual (IM70020), which shook the world of cross-border financial planning. After nearly two decades and a status quo firmly in place for 22 years under the US-UK Double Taxation Agreement (DTA), HMRC issued a view on how it would tax lump-sum distributions from US pension plans for UK residents… and it was completely at odds with the prevailing approach.

One year on from the original announcement, we are seeing the full impact of that decision unfold — and for some unfortunate American expats, dual citizens and US persons in the UK, the outlook for their retirement income could not be more different.

What changed on 12 March 2025? Why does it matter? What individuals should do to protect themselves? We cover why this is exactly the type of issue that requires an adviser with insight into taxation, investment management, and cash flow planning — three areas that are too often treated as separate specialisms within financial services.

What the 12 March 2025 Guidance Change Means for Your Retirement — And Why You Need an Adviser Who Understands Tax, Investments and Cashflow Together

The Old Position: Twenty-Two Years of Assumed Exemption

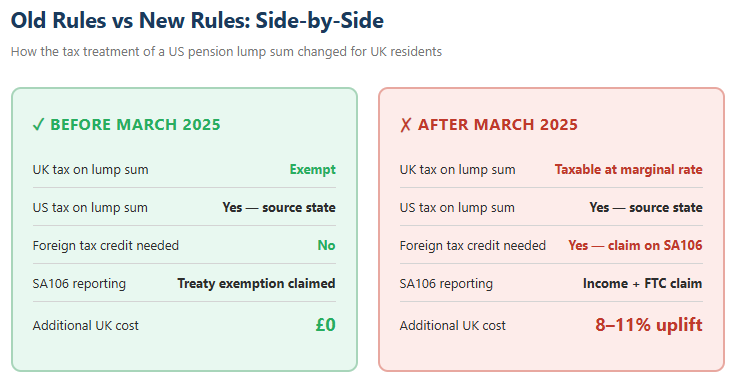

Under the terms of the US-UK Double Taxation Agreement, which were written in 2022, a pension lump sum is taxable only in the country where the pension scheme is based. If you are a UK taxpayer receiving a lump sum from a US pension plan such as a 401(k), 403(b) or traditional IRA, the Double Taxation Agreement has for many years been understood to allow the UK government to ‘stand aside’ and enable you to enjoy your pension lump sum tax-free in the UK. The US would tax the distribution as normal and your UK tax return would report the lump sum as exempt under the provisions of the treaty. This understanding was not conjecture: it was the basis on which taxpayers filed their returns, structured their pension drawdown and planned for retirement. This interpretation was not merely an informal assumption; it was the basis on which tax returns were filed, pension drawdown strategies were designed and cross-border retirement plans were built for over two decades.

Financial advisers, accountants and taxpayers were all in broad agreement that this was the position. It was predictable, straightforward and had been working perfectly for over twenty years.

Financial advisers, accountants and taxpayers were all in broad agreement that this was the position. It was predictable, straightforward and had been working perfectly for over twenty years.

2025 Change to US Pension Withdrawals: What HMRC Actually Said

HMRC’s updated guidance, published at INTM163160 in the International Manual, introduced two significant changes.

The Saving Clause: Article 1(4) Overrides Article 17(2)

The issue at the heart of the change surrounds the treaty’s saving clause (Article 1(4) of the US-UK DTA). A treaty’s saving clause permits either contracting state to tax its residents and citizens as if the treaty had never been signed, unless a specific article of the treaty is referenced as an exception in Article 1(5).

Article 17(2) – the lump sum provision – is not referenced in Article 1(5)’s list of exceptions. HMRC’s updated guidance explicitly states that it intends to begin invoking this saving clause in order to supersede Article 17(2)’s exclusive taxing rights. In effect, this means the UK intends to claim the right to tax lump sum distributions from US pensions paid to UK residents, whilst still allowing a foreign tax credit for US tax paid on the distribution.

This is a big change. Although the United States has long used the saving clause to tax its citizens on worldwide income notwithstanding treaty provisions, HMRC had previously given no indication that it would make similar claim under Article 17(2). The mere existence of the treaty, which has been in place since 2003, highlights the significance of this reversal.

Defining a “Lump Sum”: The 20% and 50% Thresholds

The second point deals with another grey area that has existed for some time. How much of a pension fund can be taken as a “lump sum” for treaty purposes? There is no definition of “lump sum” in the UK tax legislation, nor has HMRC published any guidance on this issue prior to March 2025.

HMRC has confirmed that, unless there are special reasons to justify an alternative treatment, withdrawals of 20% or more of the pension fund will generally be considered lump sums for treaty purposes. Withdrawals of 50% or more will usually be treated as a lump sum “almost certainly”. On the other hand, payments made at regular periodic intervals are less likely to be considered lump sums for treaty purposes, even if the individual has complete flexibility in deciding if and how much to take.

This issue is critical because lump sums are treated differently from periodic pension income for treaty purposes. Periodic pension payments from a US pension scheme to a UK resident are taxable in the UK as a resident, and any US tax can be claimed as a foreign tax credit. Previously, lump sums were only taxable in the US. Under HMRC’s new guidance, they may also be taxable in the UK, with relief restricted to a foreign tax credit claim.

The 2024/25 Tax Year: Caught in the Crossfire

One of the most uncomfortable aspects of the March 2025 guidance was its timing. The UK tax year 2024/25 ran from 6 April 2024 to 5 April 2025. HMRC published the updated INTM163160 guidance on 12 March 2025 — just twenty-four days before the end of that tax year. For anyone who had taken a lump sum distribution from a US pension at any point during 2024/25, the question was immediate and unsettling: does this new interpretation apply to the tax year that is almost over?

A Guidance Change, Not a Legislative Change

It is important to understand what the March 2025 publication was. It was not new legislation. It was not an amendment to the US-UK treaty. It was HMRC guidance — an update to the International Manual that represents HMRC’s interpretation of existing treaty provisions. The underlying law and treaty text have not changed since 2003.

This distinction matters because HMRC’s guidance is not, in itself, legally binding. It represents the view of the tax authority on how the law should be applied, and it carries significant weight in practice, but it is not the law itself. Individuals and their advisers are entitled to take a different view, provided they can support it with a reasonable interpretation of the treaty and domestic legislation.

Could People Rely on the Old Rules for 2024/25?

This is the central question that confronted the cross-border planning community in the weeks and months following the guidance. The answer is nuanced, and the honest position is that there is no absolute certainty either way.

- The argument for applying the old treatment in 2024/25: For twenty-two years, the prevailing and widely accepted practice was that US pension lump sums were treaty-exempt from UK tax. Returns were filed on this basis, professional advisers relied on it, and HMRC did not challenge it. An individual who took a lump sum distribution in, say, June 2024, did so in good faith reliance on an established interpretation. The guidance published on 12 March 2025 was the first time HMRC articulated this new position. To apply it retrospectively to the entire 2024/25 tax year — including transactions completed months before the guidance existed — would arguably be unfair and could be challenged on the grounds of legitimate expectation.

- The argument for applying the new treatment to the whole of 2024/25: HMRC’s position is that the guidance does not create a new rule but merely clarifies the correct interpretation of existing provisions. The saving clause at Article 1(4) has always been part of the treaty. On this view, the guidance simply explains what the law has always been, and a Self Assessment return for 2024/25 should reflect the correct legal position regardless of when the guidance was published.

What HMRC Has Said — and What It Has Not

Critically, HMRC has been silent on the question of whether it intends to apply this interpretation retrospectively. The guidance does not contain any statement about its temporal scope — it does not say it applies only to distributions made after 12 March 2025, nor does it explicitly state it applies to the whole of 2024/25 or to earlier years. Industry observers have noted that HMRC’s enquiry window for 2023/24 returns remains open, meaning returns filed on the old basis could theoretically be investigated.

This silence is itself a source of considerable unease. Several professional bodies, including the ICAEW and specialist US/UK tax firms, have called for HMRC to clarify whether the new interpretation will be applied prospectively from 2025/26 onwards, or whether it will be enforced across the full 2024/25 year and potentially earlier periods. As of March 2026, no such clarification has been forthcoming.

Practical Implications for 2024/25 Self Assessment Returns

For individuals filing 2024/25 Self Assessment returns (due by 31 January 2026 for online filing), the decision of how to report a US pension lump sum distribution taken during that year was — and remains — a judgement call that should be made with professional advice. The options available included:

- Adopting the new treatment: Reporting the lump sum as taxable UK income on the SA106 Foreign pages, claiming a foreign tax credit for US tax paid, and paying any additional UK tax due. This is the most conservative approach and eliminates the risk of a future HMRC enquiry.

- Relying on the old treatment: Reporting the lump sum as treaty-exempt, on the basis that the prevailing practice at the time the distribution was taken supported this treatment. This position carries risk, as HMRC could open an enquiry and seek to assess additional tax, potentially with interest.

- Making a protective disclosure: Some advisers recommended a middle path: reporting on the new basis but noting the circumstances and the date of the guidance in the additional information box on the return, thereby creating a transparent record of the position taken.

At Edale, we worked closely with affected clients during this period to assess each individual’s circumstances, the timing and size of any distributions taken, and their appetite for risk in relation to HMRC enquiry. There is no single right answer — the appropriate approach depends on the facts of each case. What is clear is that this is not a decision that should be made without specialist cross-border advice.

The Lesson: Guidance Can Change Overnight

Perhaps the most important takeaway from the 2024/25 experience is that reliance on “prevailing practice” is inherently fragile. For two decades, the cross-border community operated on an assumption that was never formally confirmed by HMRC. When HMRC did speak, it said something different from what everyone expected. Individuals who had built their drawdown strategy around the old interpretation found themselves exposed, and those who had not yet taken action had to rapidly reassess their plans.

This is a powerful argument for ongoing, proactive financial planning rather than reactive decision-making. If your retirement income strategy is built on tax assumptions, those assumptions need to be tested and stress-tested regularly — not simply assumed to be permanent.

UK Tax on US Pension Lump-Sum Withdrawal?

Why This Matters: The Real-World Impact on Retirement Planning

The practical consequences of HMRC’s revised position extend well beyond a change in how a line item is reported on a tax return. For UK residents with US pension savings, this guidance has the potential to fundamentally alter the economics of retirement income strategies.

Double Taxation Risk

Under the previous regime, a lump sum distribution from a US pension was taxed only in the US. The individual might pay federal (and potentially state) income tax on the distribution but would face no additional UK liability. Under the new interpretation, the UK also asserts the right to tax the distribution at the individual’s marginal rate, subject to a foreign tax credit for US taxes paid.

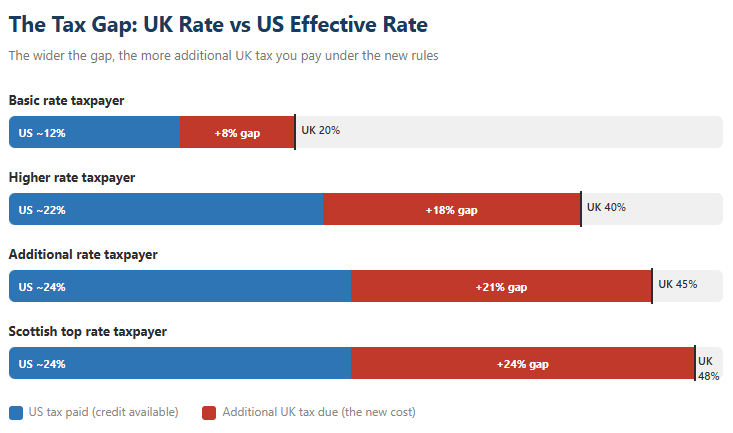

However, foreign tax credits do not always provide full relief. If the US effective tax rate on the distribution is lower than the UK marginal rate — which is commonly the case for distributions falling within lower US brackets or benefiting from US-specific reliefs — the individual will face a residual UK tax liability. Some industry estimates suggest an additional global tax cost of around 8% to 11% for affected individuals, depending on their circumstances and tax bands. For a higher-rate UK taxpayer receiving a substantial lump sum, this additional cost could be significant.

Retrospective Uncertainty

As discussed in our analysis of the 2024/25 position above, one of the most concerning aspects of the guidance is the silence on its temporal application. Tax returns filed for 2023/24 and earlier years on the basis that lump sum distributions were treaty-exempt could theoretically be reopened within HMRC’s enquiry windows. While it remains to be seen whether HMRC will actively pursue retrospective assessments, the uncertainty itself creates anxiety for those who have already taken lump sum distributions in good faith reliance on the prevailing interpretation.

Impact on Pension Drawdown Strategy

Perhaps the most important consequence is the effect on forward-looking retirement income planning. Many US/UK cross-border clients had structured their pension withdrawals around the assumption that lump sum distributions from US plans would be UK tax-free. The revised guidance means that the relative attractiveness of different withdrawal strategies has shifted.

Periodic withdrawals — structured to avoid classification as lump sums — may now be more tax-efficient in certain circumstances. The design of a drawdown strategy must consider not only the total amount to be withdrawn but also the frequency, regularity and proportion of each payment relative to the overall fund. This requires modelling across both tax jurisdictions, with attention to marginal rate thresholds, foreign tax credit availability and exchange rate assumptions.

The Broader Cross-Border Context: Pensions Under Pressure

The HMRC lump sum guidance does not exist in isolation. It arrives during a period of significant change in UK pension taxation and policy, which has particular implications for US/UK cross-border individuals.

Inheritance Tax and Pensions from April 2027

From April 2027, unused UK pension pots are expected to be brought within the scope of UK inheritance tax (IHT) for the first time. This change, announced in the Autumn Budget 2024, will end the long-standing practice of using pension funds as a tax-efficient vehicle for intergenerational wealth transfer. For cross-border families, the interaction of UK IHT, US estate tax and the estate tax treaty provisions will add yet another layer of complexity to pension planning.

Required Minimum Distributions and Cross-Border Timing

US persons with traditional IRAs and employer-sponsored plans face Required Minimum Distributions (RMDs) from age 73 under the SECURE 2.0 Act. The design of an RMD schedule for a UK resident must now account for the revised treatment of lump sums, the classification of each withdrawal, and the interaction with UK marginal rates and personal allowances. This is a multi-variable problem that demands coordinated planning across jurisdictions.

Roth Conversions and the Bigger Picture

For some individuals, the revised lump sum treatment may increase the attractiveness of Roth IRA conversions earlier in retirement, before large lump sum distributions become necessary. A Roth conversion involves paying US tax on the converted amount, but future qualified distributions are tax-free in the US. The UK treatment of Roth accounts under the treaty remains favourable in certain respects, though the position is not without complexity. The key point is that the lump sum guidance change ripples outward, affecting the relative merits of strategies that might otherwise seem unrelated.

Why You Need an Adviser Who Does All Three: Tax, Investments and Cashflow

The HMRC lump sum guidance is a perfect illustration of why cross-border retirement planning cannot be conducted in disciplinary silos. It is not a tax issue alone, nor purely an investment question, nor solely a matter of cashflow. It sits at the intersection of all three — and an adviser who is strong in only one area will inevitably miss the full picture.

The Problem with Single-Discipline Advice

The financial services industry, both in the UK and in the US, tends to organise itself around specialisms. Tax advisers focus on compliance and mitigation. Investment managers focus on asset allocation and returns. Financial planners focus on goals and cashflow projections. While each specialism is valuable in its own right, the reality of cross-border retirement planning is that these disciplines are deeply intertwined.

Consider the challenge posed by the HMRC lump sum change. A tax adviser can explain the revised treaty interpretation and calculate the tax liability on a given distribution. But they may not be well placed to assess whether the underlying investments should be repositioned before or after a withdrawal, or to model how different withdrawal sequences interact with future income needs, exchange rate movements and long-term spending plans.

An investment manager can construct an efficient portfolio and advise on asset allocation. But without deep understanding of the cross-border tax treatment of different account types, they may recommend strategies that inadvertently trigger adverse tax consequences — for example, holding UK-domiciled funds in a US brokerage account that create Passive Foreign Investment Company (PFIC) exposure, or failing to coordinate withdrawals across pension types to minimise aggregate tax.

A cashflow planner can project future income and expenditure and model different retirement scenarios. But without tax and investment expertise, the projections may rest on assumptions that are no longer valid — such as the assumption that US pension lump sums will be UK tax-free.

The Integrated Approach: What Edale Does Differently

At Edale Financial Planning, we have built our practice around the principle that cross-border financial advice must be integrated across tax, investment and cashflow disciplines. This is not a marketing claim — it is a structural feature of how we work with clients.

When we advise a client on drawing income from a US pension, we do not simply calculate the tax. We model the withdrawal across multiple scenarios, considering the classification of each payment (lump sum versus periodic), the interaction with UK marginal rates and US federal brackets, the availability of foreign tax credits, the effect on overall portfolio asset allocation and the impact on long-term cashflow sustainability. We use our proprietary cashflow modelling tools — built specifically for the US/UK cross-border context — to stress-test strategies across different market conditions, exchange rate movements and tax scenarios.

This is the kind of joined-up thinking that the HMRC lump sum change demands. A client who receives advice from a tax specialist in one meeting and an investment manager in another may end up with technically correct but practically contradictory recommendations. The tax adviser may suggest deferring distributions to manage the UK liability; the investment manager may recommend crystallising gains to rebalance the portfolio; neither may have modelled the combined effect on the client’s retirement income.

The Risk of Fragmented Advice in Practice

We have seen this fragmentation cause real damage for clients who come to us after receiving advice elsewhere. Common patterns include:

- Tax-only advice that ignores investment structure: A client was advised to take a large lump sum from a 401(k) to benefit from the (then) treaty exemption, without considering that the withdrawal forced the sale of appreciated assets at an inopportune time, crystallising losses that a phased drawdown would have avoided.

- Investment advice that ignores tax consequences: A client’s US investment manager recommended consolidating IRA accounts, triggering a taxable event that the client’s UK tax return did not account for, leading to a discovery assessment and interest charges.

- Cashflow planning on outdated assumptions: A retirement projection assumed US pension lump sums would be UK tax-free, resulting in an income plan that was unaffordable once the additional UK tax was factored in.

- Failure to coordinate US and UK pension strategies: A client was advised on their UK SIPP drawdown without reference to their US IRA obligations, leading to unnecessary income bunching and higher aggregate tax across both jurisdictions.

These are not hypothetical scenarios. They are the lived experience of cross-border clients navigating a system that was already complex before the March 2025 guidance made it more so.

Edale’s US Pension Distribution Tax Calculator: Navigating the New World

In direct response to the March 2025 guidance change, Edale has developed a dedicated US Pension Distribution and Withholding Tax Calculator — a practical tool built specifically to help cross-border clients and their advisers understand the tax implications of withdrawals from US pension plans under the revised HMRC framework. This is not a generic tax tool; it has been designed from the ground up for the unique complexities of US/UK cross-border pension taxation.

What the Calculator Does

The Edale calculator addresses the central question that every UK-resident US pension holder now faces: how much tax will I actually pay, across both jurisdictions, on a given pension distribution? It brings together the key variables that determine the answer, including elements that are routinely overlooked by generic tax software and even some professional advisers.

Voluntary Withholding Tax: Getting the US Side Right

A critical starting point for any US pension distribution to a UK resident is the question of US withholding tax. When a distribution is made from a 401(k), 403(b), traditional IRA or similar US plan, the custodian or plan administrator will typically withhold federal income tax at source. The default withholding rate for eligible rollover distributions is 20%, although the individual may elect a different rate or, in certain circumstances, opt for voluntary withholding at a rate that better reflects their actual US tax liability.

Getting this right matters enormously. Under the revised HMRC treatment, the UK will allow a foreign tax credit only for US tax that has actually been paid. If the US withholding rate is set too low — or if the individual has elected zero withholding via a Form W-8BEN for what they believed would be a treaty-exempt distribution — the foreign tax credit available on the UK return will be correspondingly smaller, and the residual UK tax bill will be larger.

Conversely, if the US withholding rate is set unnecessarily high, the individual has overpaid in the US and must wait to reclaim the excess through their US tax return, creating a cashflow cost. The Edale calculator helps clients model the optimal voluntary withholding rate by comparing scenarios: it shows the total global tax payable at different US withholding percentages and identifies the rate that minimises both the overall tax cost and the timing mismatch between US payment and UK credit.

HMRC Official Exchange Rates: Converting Your Distribution to Sterling

One of the most commonly misunderstood aspects of cross-border pension taxation is the currency conversion. HMRC requires that foreign income — including US pension distributions — be reported on the Self Assessment return in pounds sterling. The exchange rate used for this conversion directly affects both the amount of UK taxable income and the value of the foreign tax credit claimed.

HMRC publishes official exchange rates, and its general position is that income should be converted at the rate prevailing on the date the income arises. For a lump sum distribution, this means the spot rate on the date the distribution is paid. For periodic payments, individuals may use either the rate on each payment date or a consistent recognised average rate for the period, provided they apply the same method consistently.

The Edale calculator integrates HMRC’s published exchange rates directly, pulling the appropriate USD/GBP rate for the distribution date or period. This removes the guesswork and the risk of using an incorrect or inconsistent rate — a surprisingly common error that can trigger HMRC correspondence and, in some cases, adjustments to the tax payable. The calculator also shows the effect of exchange rate movements on the net after-tax income, so clients can see how currency risk interacts with their withdrawal strategy.

The Foreign Tax Credit Regime: How It Works Under the New Rules

The foreign tax credit (FTC) mechanism is the linchpin of the revised tax treatment. Under the old interpretation, no UK tax was due on a lump sum distribution, so the FTC was irrelevant. Under HMRC’s new position, the lump sum is taxable in the UK at the individual’s marginal rate, but relief is available for US tax paid on the same income, claimed through the SA106 Foreign pages of the Self Assessment return.

However, the FTC is not a simple dollar-for-pound offset. The credit is limited to the lower of the actual US tax paid (converted to sterling) and the UK tax attributable to that income. In practice, this means:

- If the US effective tax rate on the distribution is lower than the UK marginal rate, the individual pays the difference to HMRC. This is the most common scenario and is where the estimated 8–11% global tax uplift arises.

- If the US effective tax rate is higher than the UK marginal rate, the excess US tax cannot be credited against other UK income — it is simply wasted, unless it can be carried forward or reclaimed from the IRS.

- The interaction with US state income tax adds further complexity. Some US states tax pension distributions; the credit position for state-level tax must be considered separately.

- The timing of payment matters. The UK tax year (6 April to 5 April) and the US tax year (calendar year) do not align. A distribution in January 2026 falls in the 2025/26 UK tax year but the 2026 US tax year. The FTC must be claimed in the UK year in which the income arises, using the US tax paid or payable on that income — which may not be finalised until the US return is filed months later.

The Edale calculator models all of these variables. It takes the gross distribution amount in USD, applies the appropriate HMRC exchange rate, calculates the UK tax liability at the individual’s marginal rate, offsets the US tax paid (converted at the same rate), and shows the net residual UK tax due. It also models the effect of different distribution amounts on the individual’s UK tax band — because a large lump sum may push the individual into a higher marginal rate, increasing the gap between the US and UK rates and therefore the additional UK cost.

Putting It All Together: A Worked Example

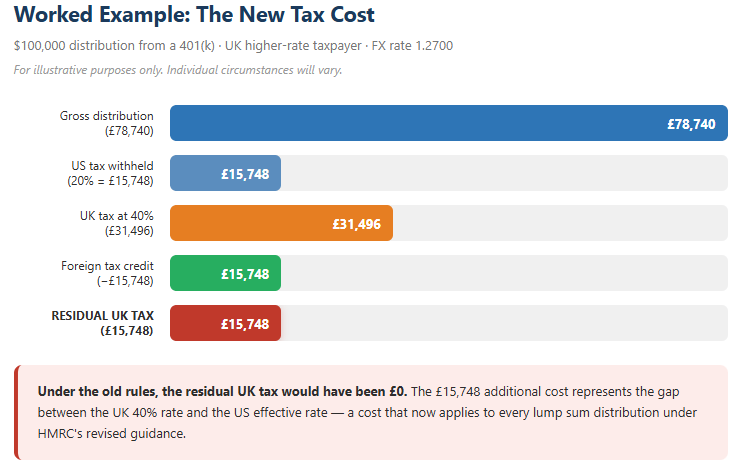

Consider a UK resident who is a US citizen with a 401(k) valued at $500,000. They wish to take a distribution of $100,000 in a single payment. Under the revised HMRC guidance, this is likely to be classified as a lump sum (20% of the fund). The Edale calculator would model the following:

- US federal withholding: At the default 20% rate, $20,000 is withheld. The actual US tax liability will depend on the individual’s total US income and filing status — the calculator models this.

- HMRC exchange rate conversion: Assuming a rate of 1.2700 on the distribution date, the gross distribution is £78,740 and the US tax paid converts to £15,748.

- UK tax calculation: If the individual is a higher-rate taxpayer, UK tax at 40% on the £78,740 would be £31,496. After the foreign tax credit of £15,748, the residual UK tax due is £15,748 — an additional cost that did not exist under the old interpretation.

- Optimisation: The calculator can then model what happens if the same $100,000 is taken as four quarterly payments of $25,000 instead. If each payment represents only 5% of the fund, it may be classified as periodic income rather than a lump sum — though the tax treatment under the treaty still results in UK taxation for periodic payments. The key difference may lie in the interaction with UK tax bands and the ability to spread income across tax years.

Why a Calculator Matters in This New Environment

The HMRC guidance change has made US pension withdrawals for UK residents significantly more complex. What was once a straightforward treaty exemption is now a multi-step calculation involving US withholding rates, HMRC exchange rates, foreign tax credit limits, UK marginal rate thresholds and timing considerations across mismatched tax years.

Without a tool that brings these variables together, it is extremely difficult for an individual — or even a generalist financial adviser — to assess the true after-tax cost of a pension distribution. The Edale calculator was built to fill this gap. It is one of several proprietary tools that Edale has developed for cross-border clients, alongside our cashflow modelling system, risk profiling framework and portfolio analysis suite. Together, they form the analytical backbone of our integrated advice process.

If you would like to use the calculator or understand how it applies to your personal situation, please get in touch. We offer a no-cost initial consultation for US/UK cross-border clients and can walk you through the numbers for your specific circumstances.

Practical Steps: What to do with US Pension withdrawals from 2026 onward

If you are a UK resident with US pension savings, the one-year anniversary of the HMRC guidance change is an appropriate moment to review your position. The following steps are relevant regardless of whether you have already begun drawing on your US pension or are still in the accumulation phase.

1. Review Your Current Drawdown Strategy

If you are currently taking distributions from a US pension, assess whether any payments could be classified as lump sums under HMRC’s new framework. Consider the proportion of the fund being withdrawn, the regularity of payments and whether the withdrawal pattern could be restructured to fall more clearly within the periodic payment classification.

2. Assess Your Foreign Tax Credit Position

Understand how the US tax paid on any lump sum distribution interacts with the UK liability. Foreign tax credits are not automatic — they must be claimed, and the calculation can be complex where income from multiple sources and jurisdictions is involved. Ensure your Self Assessment return correctly reflects the revised treatment.

3. Model Your Retirement Income Across Both Jurisdictions

This is where integrated cashflow planning becomes essential. A multi-year projection that models different withdrawal strategies, tax rates, exchange rate scenarios and market conditions will give you a much clearer picture of the options available. This should encompass all retirement income sources — US pensions (401(k), IRA, Roth), UK pensions (workplace schemes, SIPPs), US Social Security, UK State Pension and any investment income.

4. Consider the Interaction with Future UK Tax Changes

With IHT on unused pension pots potentially arriving in April 2027, and ongoing speculation about the future of the 25% tax-free lump sum in UK pensions, any withdrawal strategy should be stress-tested against a range of possible future policy changes. Building flexibility into your plan is as important as optimising for today’s rules.

5. Take Professional Advice from an Integrated Cross-Border Specialist

This is not a situation where generic financial advice will suffice. The interaction of US and UK tax law, treaty provisions, investment structures and retirement income planning requires an adviser with deep expertise across all of these areas. A firm that specialises in tax compliance alone, or investment management alone, or UK domestic financial planning alone, will not be equipped to navigate the full range of issues.

How Edale Supports US/UK Cross-Border Clients

Edale Financial Planning was founded in 2014 with a specific focus on the financial planning needs of US citizens, dual nationals and US persons living in the UK. Cross-border advice is not an add-on to our business — it is the core of what we do.

Our founder, Lawrie Chandler, has spent over a decade advising on US/UK cross-border investing and has worked with expatriates and internationally mobile individuals since 2000. The firm is FCA-regulated and operates from a foundation of deep knowledge in cross-border taxation, FATCA compliance, US/UK pension structures and the practical realities of building and maintaining a financial life across two jurisdictions.

We work with clients at every stage of their cross-border journey: from those who have recently relocated from the US to the UK, to long-established dual citizens planning for retirement, to individuals in the Middle East and elsewhere who hold US and UK financial interests. Our services span the full range of cross-border financial planning needs, including:

- US/UK pension drawdown strategy and tax-efficient income planning

- IRA, Roth IRA and 401(k) management for UK residents

- Cross-border cashflow modelling and retirement projections

- FATCA-compliant investment portfolios and PFIC avoidance strategies

- UK SIPP and workplace pension advice for US persons

- Estate planning and the interaction of UK IHT with US estate tax

- Proprietary tools, including the US Pension Distribution Tax Calculator, Cashflow Modeller and Portfolio X-Ray

We believe that financial advice should be accessible to everyone, regardless of portfolio size or the complexity of their circumstances. That is why Edale has no minimum investment requirement and offers free initial consultations. If you would like to discuss how the HMRC lump sum guidance affects your personal situation, or if you want to ensure your retirement income plan is built on current, integrated advice, we are here to help.

Conclusion: One Year On, the Case for Integrated Advice Is Stronger Than Ever

The HMRC guidance of 12 March 2025 was a wake-up call for the US/UK cross-border community. It exposed the fragility of long-held assumptions, highlighted the importance of staying current with evolving interpretations of treaty law, and demonstrated beyond doubt that retirement planning for cross-border individuals cannot be reduced to a single discipline.

Tax knowledge alone is not enough. Investment expertise alone is not enough. Cashflow modelling alone is not enough. What is needed is an adviser who can hold all three together, who understands the specific dynamics of the US/UK cross-border context, and who can translate complexity into a clear, actionable plan for retirement.

The 2024/25 tax year showed us what happens when guidance changes mid-stream and individuals are caught without a plan. The Edale US Pension Distribution Tax Calculator is one practical response to that challenge — but it is part of a much broader philosophy: that cross-border clients deserve advice that is integrated, current, and built around their specific circumstances.

At Edale, that is exactly what we do. If you are a US citizen, dual national or US person living in the UK and you have questions about your pension, your tax position or your retirement income, we would welcome the opportunity to speak with you.