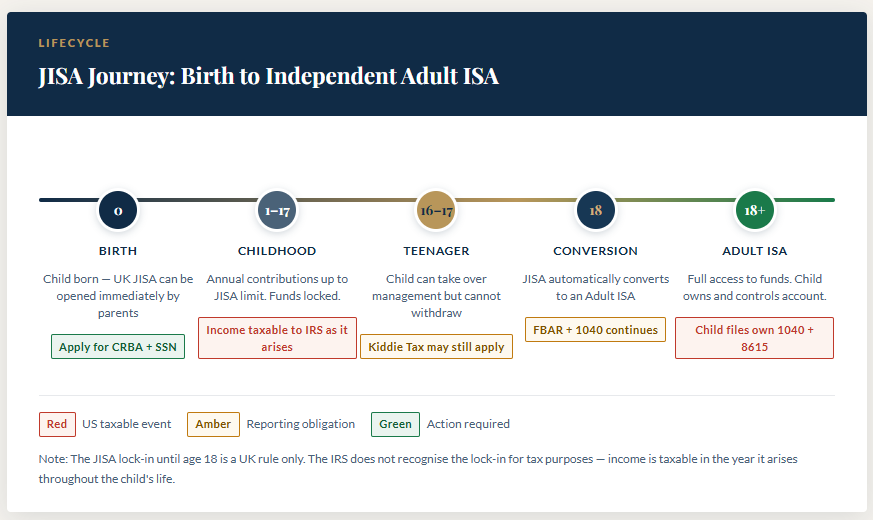

Opening a Junior ISA (JISA) or ISA for a child is one of the most common forms of savings for US persons residing in the UK. However, as the US taxes on citizenship rather than residency, these “tax-free” UK savings accounts are completely transparent – and typically taxable – to the IRS.

Here is a guide for parents on the technical standards, reporting requirements, and “Kiddie Tax” rules for UK investment accounts held in the names of US dependent children.

The Core Conflict: UK Tax-Free vs. US Taxable

The UK government views ISAs as a tax wrapper. The US-UK Tax Treaty does not view ISAs as pension or retirement accounts. The IRS considers an ISA to be a regular brokerage account. You must report all interest, dividends and capital gains earned inside your ISA every year on your US tax return (Form 1040). Junior ISA (JISA): Funds are locked until the child is 18. However, for US tax purposes, the income is still generally “taxable as it arises”.

American parents or not

If your child is a US citizen by birth but their parents are not US persons, then they will only have a tax return filing requirement if their total taxable income is above the de minimis (2025 tax year (filing in 2026) this is $15,750), or if they owe any ‘special taxes’, such as alternative minimum tax, self-employment tax, Passive Foreign Investment Company tax, etc.

Children with at least one US parent are generally considered US citizens (and thus tax residents) subject to worldwide taxation, regardless of where they live. They are considered dependents if they are under 19 (or under 24 and full-time students) and receive more than half their support from the parent.

Securing a Social Security Number (SSN) for Your Child

Claiming the lucrative Child Tax Credit requires your child to have a US Social Security Number issued before the tax deadline. If your child was born in the UK, this does not happen automatically.

Parents must proactively apply for a Consular Report of Birth Abroad (CRBA) and a US passport at the US Embassy in London or a consulate. You can apply for the child’s SSN concurrently using Form SS-5. Because wait times for embassy appointments and SSN processing can take several months, expecting parents should initiate this process as soon as possible after birth.

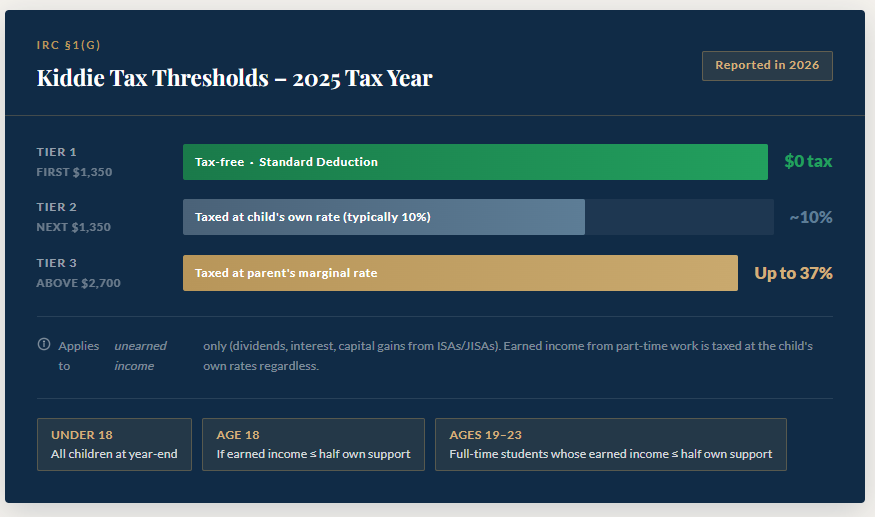

The “Kiddie Tax” Standards (2025-2026)

To prevent parents from shifting assets to children to pay lower tax rates, the IRS applies the Kiddie Tax (Internal Revenue Code Section 1(g)). For the 2025 tax year (reported in 2026), the thresholds are:

| Income Tier | Tax Treatment |

| First $1,350 | Tax-free (covered by the child’s standard deduction) |

| Next $1,350 | Taxed at the child’s marginal rate (usually 10%) |

| Above $2,700 | Taxed at the parent’s marginal rate (up to 37%) |

Note: These rules apply to “unearned income” (dividends, interest, capital gains). If the child has a part-time job, that “earned income” is taxed at their own normal rates.

Clarifying the Kiddie Tax Age Limits

The Kiddie Tax doesn’t just apply to young children; it can also apply to dependents well into young adulthood. The IRS rules state that the Kiddie Tax applies to:

- All children under the age of 18 at the end of the tax year.

- 18-year-olds whose earned income does not exceed half of their own support costs.

- Full-time students aged 19 to 23 whose earned income does not exceed half of their own support costs.

As long as your child falls into one of these categories and crosses the unearned income thresholds, their investment income will be taxed at your (the parent’s) highest marginal tax rate.

Navigating Currency Conversion for US Reporting

When assessing whether your child’s accounts meet the FBAR and tax reporting thresholds, you must convert the Great British Pound (GBP) balance into US Dollars (USD).

Do not use a random daily exchange rate. For FBARs, the Financial Crimes Enforcement Network (FinCEN) explicitly requires taxpayers to use the official US Treasury Department’s year-end exchange rate published on December 31st. Similarly, all unearned income (dividends and interest) generated throughout the year must be converted into USD using appropriate IRS exchange rates for that tax year before being entered onto Form 1040, Form 8814, or Form 8615.

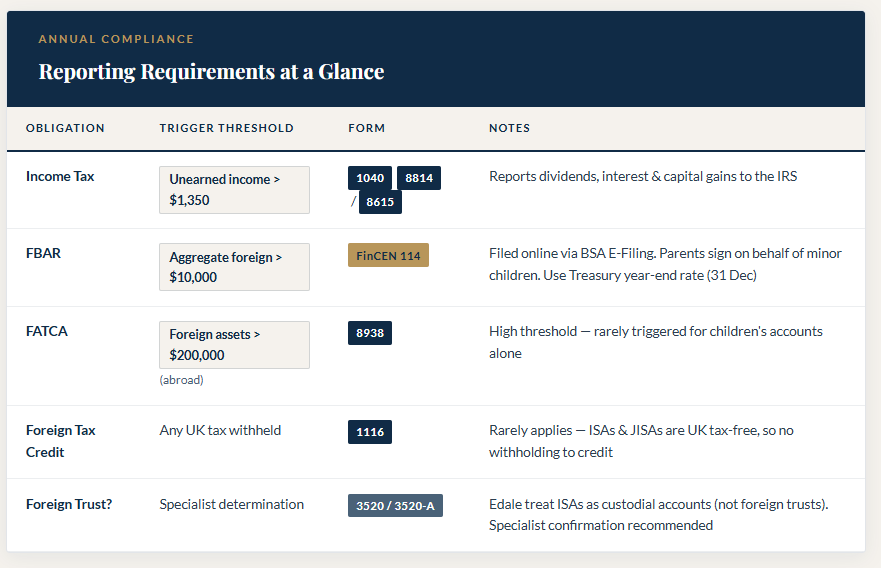

Mandatory Reporting Forms

A parent must ensure the following forms are filed if thresholds are met:

- Form 1040 (Schedule B & D): To report the actual interest, dividends, and gains.

- FBAR (FinCEN Form 114): If the total value of all foreign accounts (including the JISA) exceeds $10,000 at any point in the year.

- Form 8938 (FATCA): If foreign assets exceed certain thresholds (usually $200,000+ for expats, but varies by filing status).

- Form 3520/3520-A: Some practitioners argue a JISA is a “Foreign Trust,” requiring these complex forms. While most now treat ISAs as custodial accounts, you should verify this with a specialist. Edale do not view ISAs as a foreign trust, as it’s purely a tax wrapper.

Child Tax Credit (CTC) Relief

On the bright side, US parents in the UK can often claim the Child Tax Credit.

- Amount: For 2025, the credit is up to $2,200 per qualifying child under age 17.

- Refundability: Up to $1,700 of this can be refundable (the “Additional Child Tax Credit”), meaning you may receive a check from the IRS even if you owe $0 in US tax.

- Requirement: The child must have a US Social Security Number (SSN) issued before the tax filing deadline.

Technical Standards for Parents

If you are managing a child’s UK account, you must navigate these specific IRS authorities:

- IRC §1(g) (The Kiddie Tax): This is the primary statute. It mandates that a child’s “net unearned income” above a threshold is taxed at the parent’s marginal rate.

- IRS Publication 929: The definitive guide for “Tax Rules for Children and Dependents.

- Form 8814 vs. Form 8615: Form 8814: Used if you elect to report your child’s income on your return (only if their income is between $1,350 and $13,500).

- Form 8615: Used if the child files their own return (mandatory if unearned income exceeds $13,500).

- Treasury Reg. §301.7701-4(a): This defines what a “trust” is. Most experts argue that a JISA is a custodial account (like a UTMA/UGMA), not a foreign trust, which spares you from the nightmare of Forms 3520/3520-A.

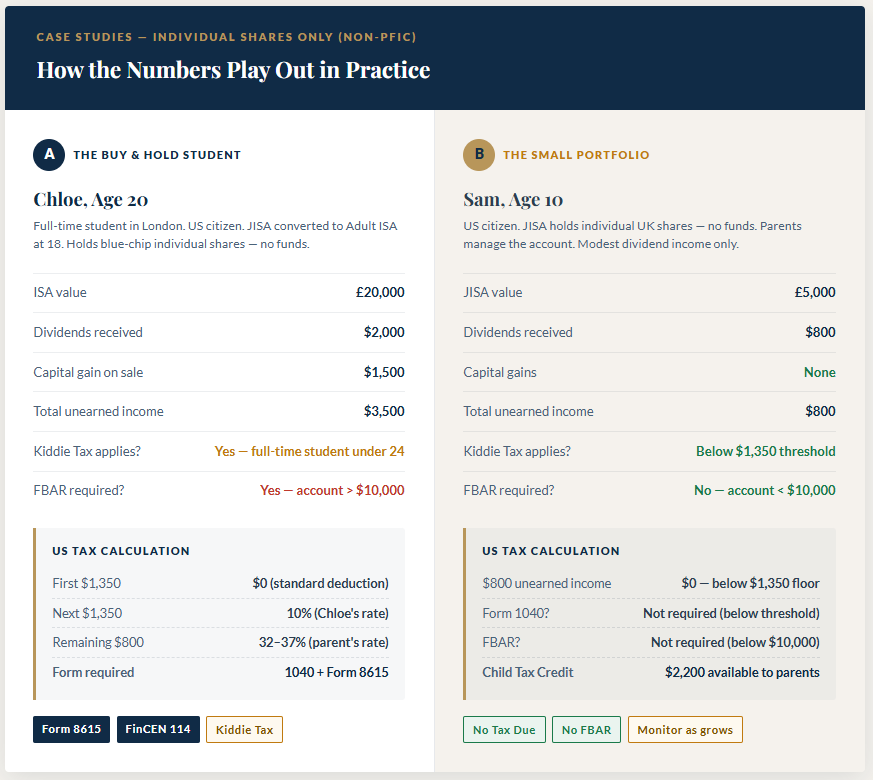

Case Studies (Non-PFIC / Shares Only)

Case A: The “Buy and Hold” Student (Age 20)

Situation: Chloe is 20, a full-time student in London, and a US citizen. Her JISA converted to an Adult ISA at age 18. She holds £20,000 in individual blue-chip shares (no funds). In 2025, she receives $2,000 in dividends and sells one stock for a $1,500 gain.

- Total Unearned Income: $3,500.

- US Tax Calculation: * First $1,350: Tax-free (Standard Deduction).

- Next $1,350: Taxed at Chloe’s rate (10%).

- Remaining $800: Taxed at her parents’ top marginal rate (e.g., 32% or 37%).

- Reporting: Chloe must file her own Form 1040 (with Form 8615) and an FBAR because her account exceeds $10,000.

Case B: The “Small Portfolio” Election

Situation: Sam is 10. His JISA holds £5,000 in individual UK shares. He earns $800 in dividends.

- US Tax Calculation: Because $800 is below the $1,350 threshold, Sam owes $0 in US tax.

- Reporting: Even though no tax is due, if the account value (converted to USD) exceeded $10,000 at any point, Sam’s parents must file an FBAR on his behalf. No Form 1040 is required because income is below the filing threshold.

Reporting Matrix for UK Accounts

As the “responsible adult,” you are looking at the following annual requirements:

| Requirement | Threshold | Form | Note |

| Income Tax | Unearned income > $1,350 | 1040 + 8814/8615 | Reports dividends/gains to the IRS. |

| FBAR | Aggregate foreign total > $10,000 | FinCEN 114 | Filed online via BSA E-Filing System. |

| FATCA | Total foreign assets > $200k (abroad) | Form 8938 | High threshold for most children. |

| Foreign Tax Credit | Any UK tax withheld | Form 1116 | Rarely applies to ISAs as the UK doesn’t tax them. |

Where to Find Official Guidance

To verify these rules or hand them to a local accountant, refer to these specific IRS sources:

- IRS.gov – Kiddie Tax Information: Explains the age limits (under 19, or under 24 for students).

- Instructions for Form 8615: Detailed worksheets for calculating the tax at the parent’s rate.

- FinCEN FBAR Guidance: Specifically look for “Reporting for Minors”—parents generally sign for the child.

- The US-UK Tax Treaty: Review Article 17/18 (Pensions) to see why ISAs are excluded from treaty protection.