HMRC has just rewritten the rules on US pension withdrawals for UK residents. For UK-resident individuals receiving lump-sum distributions from US pensions (e.g., 401(k)s, traditional IRAs), individuals now pay more tax. In a long-standing interpretation, these US-source lump sums have generally been considered exempt from UK tax for the past ~24 years. Under the 2001 US–UK tax treaty, Article 17(2) (reserved for the country where the payment arises). HMRC’s new internal guidance says otherwise: now the UK has determined it will tax US-source lump sums to UK residents too, alongside the US, with any double tax relief via foreign tax credit.

Below, we explain what changed (in plain English, the old and new side-by-side), why this matters, and what to do about it.

The Short Version

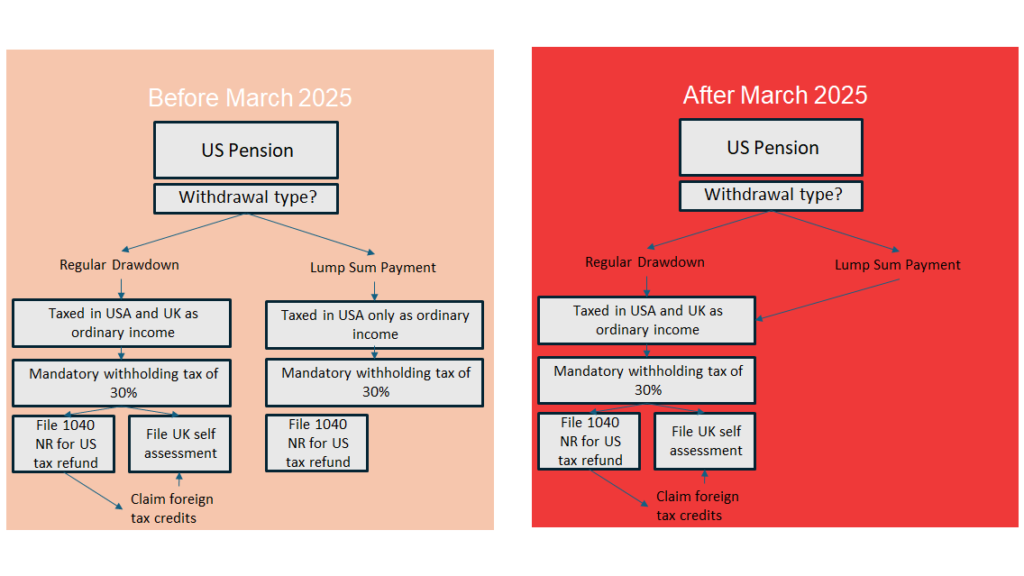

- What changed? HMRC’s March 2025 updates to its International Manual interpreting the treaty’s “saving clause” so that the UK may tax US-source pension lump sums paid to UK residents (elimination of double taxation is via claiming foreign tax credit relief).

- What did most people do before? Treat US-source pension lump sums to UK residents as taxable only in the US (therefore not taxable in the UK) under Article 17(2).

- What’s the impact now? Many UK residents will face additional UK tax on top of US withholding (subject to foreign tax credit). The size of the UK “top-up” depends on the taxpayer’s UK marginal rate.

A 24-Year Backdrop: Why UK Pension Tax Change for US pensions Is Big

The US–UK treaty wassigned in 2001 and entered into force in 2003. For about 24 years, Article 17(2)’s carve-out for lump sums was widely read to give exclusive taxing rights to the country where the pension payment arose (e.g. the US for a 401(k)). HMRC’s 2025 guidance departs from that reading by giving effect to Article 1(4) “saving clause”—a clause previously long understood as US-facing—so that both states may tax their residents, with double tax relief balancing the result.

Professional commentary and trade press flagged the change immediately, noting HMRC’s new stance and planning consequences for UK residents with US pensions. Few financial advisers, though, are on top of the solution that we are (secret: it’s here in Roth IRA conversions).

Old Regime vs New Regime (Side-by-Side)

Old Regime (pre-March 2025 interpretation)

- Treatment: US-source lump sums (e.g. cashing out a 401(k)/IRA in one or a few payments) to a UK resident are generally treated as taxable only in the US, not in the UK, under Article 17(2).

- Practical impact: UK residents often faced US withholding and US tax on the lump sum, but no UK tax; treaty relief planning focused on US rules and optimal timing.

New Regime (HMRC guidance from March 2025)

- Treatment: HMRC reads the saving clause to allow the UK to tax its residents on US-source lump sums as well, with double tax relief for US tax already paid. The result can be a UK top-up where UK rates exceed the US effective rate.

- Practical impact:

- Additional UK tax exposure for higher-rate and additional-rate taxpayers (rest-of-UK up to 45%, Scotland up to 48%), after crediting US tax. [USTAXFS]

- Definition of “lump sum” matters (frequency/format of withdrawals). HMRC’s updated commentary indicates it is considering how a lump sum is characterised, which influences which treaty article bites. Expect case-by-case analysis.

- Compliance: UK self-assessment now needs to reflect the distribution and the foreign tax credit position. [BHP, Chartered Accountants]

How HMRC Justifies the Shift on US Pension Taxing

HMRC’s manual updates indicate that, even though Article 17(2) grants exclusive taxing rights to the state where the lump sum arises, the treaty’s Article 1(4) saving clause “in effect overrides” that exclusivity for residents (and US citizens), unless a provision is explicitly carved out in Article 1(5). In HMRC’s view, that means both jurisdictions may tax UK residents, with double tax relief preventing double taxation.

Planning Implications for UK Residents with US Pensions

- Mind the rate differential

If the US withholds, say, 20–30% on the lump sum but your UK marginal rate is 40–45% (or 48% in Scotland), expect a UK top-up after foreign tax credit. Conversely, basic-rate UK taxpayers might see little to no top-up. - Re-evaluate “lump sum” vs staged withdrawals

HMRC’s focus on what counts as a lump sum means payment frequency and structure can change the treaty analysis. Spreading withdrawals may alter tax timing and effective rates, but it won’t, by itself, remove the UK tax exposure under the new stance. - Coordinate with UK lump-sum allowances (for UK pensions)

The UK abolished the Lifetime Allowance and introduced lump-sum allowances from 6 April 2024, which affect UK pensions. These do not directly affect US pension lump sums, but they matter for overall cash flow and sequencing if you’re drawing both UK and US pensions. - Model foreign-tax-credit mechanics

Double tax relief is your friend—but credits can be capped and do not always eliminate all UK liability. Modelling US withholding vs UK marginal rates ahead of time is now essential. - Watch for retroactivity and edge cases

Commentary notes lingering questions about effective dates and whether HMRC applies this reading prospectively or to past distributions. Keep records and seek advice before large withdrawals.

Frequently Asked Questions

Does lump sum UK tax change affect periodic US pension income (not lump sums)?

Periodic pension income has long been taxable in the country of residence (the UK, if you’re UK-resident), with credit relief as appropriate. The 2025 shift is significant, specifically because it undermines the previous UK non-taxation expectation for US-source lump sums.

What if I already planned a 100% cash-out this year?

Run a revised projection: estimate US withholding and your UK marginal rate, then compute the UK top-up after credit. Staging withdrawals, altering timing (e.g. across tax years), or coordinating with other income may reduce the blended effective rate.

Does this change Roth IRA rules?

The HMRC update addresses taxable US plans and the treaty reading for lump sums. Roth issues (qualified vs non-qualified distributions, treatment under Article 17 and domestic law) require separate analysis and remain complex. The key takeaway: don’t assume past rules still hold without a fresh treaty/domestic-law review. The general consensus among professionals is to confirm your individual specialist advice.

Action Checklist (What to Do Now)

- Record your US pension types (401(k), traditional IRA, Roth IRA, previous employer plans) and planned withdrawal style (single lump vs phased).

- Re-run tax projections using the new HMRC stance—build in UK top-up cases with foreign tax credit limits.

- Sequence drawings with other income (salary, dividends, UK pension crystallisations) to manage UK marginal rates.

- Document treaty positions in your UK return and keep proof of US tax paid to support the foreign tax credit.

- Monitor HMRC’s International Manual for further clarifications and any examples they add.

For UK-resident holders of US pensions, lump sums are no longer comfortably outside UK tax. The saving clause interpretation means both the US and the UK can now tax the payment—with credit relief to mitigate double tax—often leaving a UK top-up for higher-rate taxpayers.

If you are planning a distribution, recalibrate now, before you pull the trigger.