A Roth IRA functions as a retirement account which provides significant tax advantages. It has no UK equivalent but its advantages make it worth considering for retirement and retirement planning. Contributions to the account come from after-tax dollars, but invested funds grow without taxation, and qualified withdrawals are tax-free both in the USA and the UK. The article provides strategies for making tax-efficient withdrawals and conversions by using Roth IRAs. People who are age 50 or older should definitely be familiar with this product as they plan retirement or are already retired. Read our other US UK Financial Advice blogs to learn about how Roth IRAs can help in wealth accumulation. The use of Roth IRAs for tax-efficient incomes in the UK and USA si complex and the rules change so use an adviser for this getting started and journey towards qualified distributions.

Roth IRA in the UK

ROTH IRAs do not have a UK equivalent. Comparing them to an ISA is like saying third cousins are related and the same; they’re not.

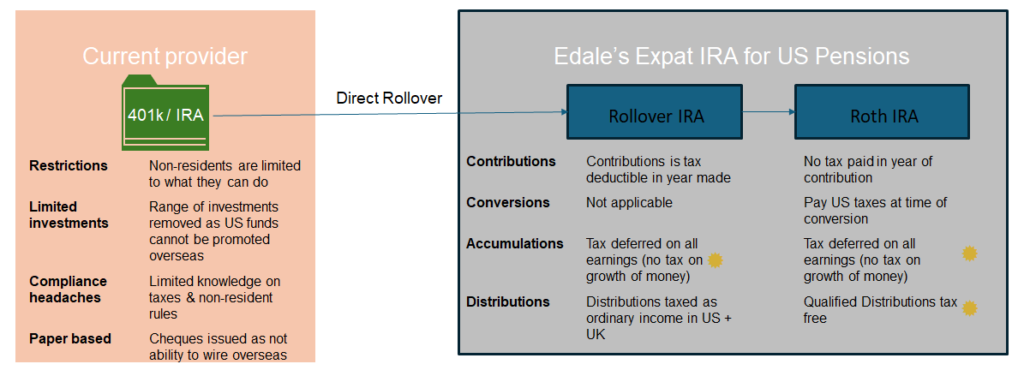

We are frequently asked about the tax implications of a Roth IRA when retiring and taking distributions in the UK. Also, Roth IRAs can be used for efficient financial planning when having a 401k or traditional IRA, where conversions can be made to create tax-efficient distributions from US Pensions. The unique tax treatment of Roth IRAs makes them an effective part of retirement planning for the UK.

Can a UK Resident Use a Roth IRA?

Anyone with a US Social Security Number (from now or in the past) or ITIN can then open a Roth IRA and/or IRA to transfer 401ks or convert assets into a Roth IRA. Anyone is eligible to convert regardless of their income or tax filing status.

Technical explanation of why Roth IRA are tax free in the US and UK

In addition to the double taxation treaty Technical Guidance produced by the tax authorities, explains that Roth IRA withdrawals are tax emplt in the UK and US. The US-UK treaty has specific provisions that affect the treatment of Roth IRAs held by UK residents.

The U.S. Treasury Department’s Technical Explanation on the US-UK Tax Treaty provides specific clarification. The technical explanation is an official guide to the Convention. It reflects the policies behind particular Convention provisions and understandings reached regarding its interpretation and application.

For example, a distribution from a U.S. “Roth IRA” to a U.K. resident would be exempt from tax in the United Kingdom to the same extent the distribution would be exempt from tax in the United States if it were distributed to a U.S. resident. The same is true with respect to distributions from a traditional IRA to the extent that the distribution represents a return of nondeductible contributions. Similarly, if the distribution were not subject to tax when it was “rolled over” into another U.S. IRA (but not, for example, to a U.K. pension scheme), then the distribution would be exempt from tax in the United Kingdom.

IRS Treaty-UK-Protocol-TE-7-22-2002

Here is the UK technical guidance on Roth IRA taxation.

Article 17 provides for the taxation of pensions and other similar remuneration only in the state of residence of the beneficial owner. For this purpose, a payment is treated as a pension or other similar remuneration if it is a payment under a pension scheme, as defined at Article 3(1)(o).

IRAs

Contrary to this general rule, the residence state, under paragraph 1(b), must exempt from tax any amount of such pensions or other similar remuneration that would be exempt from tax in the State in which the pension scheme is established if the recipient were a resident of that State. Thus, for example, a distribution from a US Individual Retirement Arrangement or “IRA” to a UK resident will be exempt from tax in the UK to the same extent that the distribution would be exempt from tax in the US.

HMRC’s Double Taxation Relief Manual (https://www.gov.uk/hmrc-internal-manuals/double-taxation-relief/dt19853)

Get Your Personalised Tax Strategy Report for US Pension withdrawals

Enter your details below to see how different withdrawal strategies will be taxed—and discover an optimised plan for minimizing your tax bill.

Tax-free IRA conversions for US Expats

There is a valid route to convert to a Roth IRA without paying any US taxes on conversion. They are only available to a particular group of US expats: those using the Foreign Earned Income Exclusion for US expat taxes. You may be able to convert a portion of 401k or traditional IRA into a Roth IRA.

Understanding Tax-Free Roth Conversions for US Expats

Although expats face complex US tax requirements, they also gain unique opportunities such as tax-free Roth conversions. American expats must submit tax returns to the IRS every year, regardless of where they reside. The Foreign Earned Income Exclusion (FEIE) allows expatriates to deduct up to $30,000 (2025) of foreign-earned income per person for the year 2025 while providing substantial benefits. Expats can optimise their tax strategy by combining standard deductions ($15,000 for single filers in 2025) with other benefits.

Qualifying Criteria for Tax-Free Roth Conversions

Expats aiming for a tax-free Roth conversion must meet specific requirements to qualify. Ensure your foreign income does not surpass the sum of the FEIE and Housing Exclusion limits. Any amount that surpasses the limit must not exceed the standard deduction amount. You must maintain all other non-excluded income below your total deductions. You must have access to either an existing or newly created Roth IRA account. Tax-free IRA or 401(k) to Roth IRA conversions become possible within the limits of your unused deductions when you meet these conditions.

US expats experience numerous advantages through Roth IRA accounts

Retirement planning for expats achieves unmatched flexibility through Roth IRA accounts. Investments in these accounts achieve tax efficiency and protect earnings from future taxes, establishing enduring financial security. If you don’t know much about Roth IRAs, get in touch with the US. They are ideal for US expats who reside in the UK and other places where Roth IRA distributions are recognised as not taxable in the Dual Taxation Agreement.

Do you qualify for tax-free Roth IRA conversions?

Take our questionnaire to see if you qualify for tax-free pension conversions.

Step 1: Are you a U.S. citizen or green card holder (U.S. taxpayer)?

Backdoor ROTH IRA conversion for UK residents

Expats can use a Backdoor Roth IRA as a legal and strategic way for a high earner, where foreign income is way above the MAGI limit, to enjoy the benefits of a Roth IRA without income limits standing in the way. Using Non-deductible Traditional IRA contribution – The original contribution’s lack of tax relief ensures that the conversion process remains tax-exempt while moving funds into the Roth IRA as if they had been directly contributed. Hence the term ‘backdoor’ Roth IRA contribution.

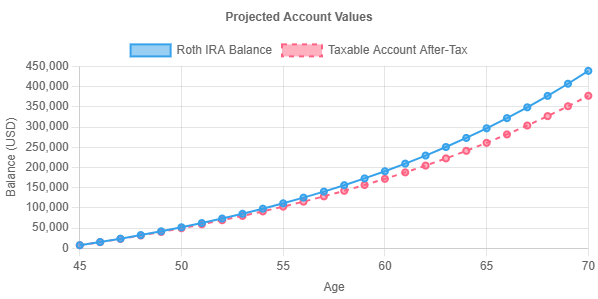

Contributing the current maximum of $7,000 per year starting at age 45 with an expected annual return of 6.0% and a capital gains tax rate of 24.0% (which is the highest CGT level in the UK).

At age 55 (after 10 years):

- Roth IRA balance: $111,090

- Taxable account after-tax: $102,908

- Roth advantage: $8,182 (8.0%)

At age 70:

Illustration of the tax advantages of Backdoor Roth IRA.

- Roth IRA balance: $438,940

- Taxable account after-tax: $377,275

- Roth advantage: $61,666 (16.3%)

Types of withdrawals from a Roth IRA

There are two distribution categories for Roth IRAs which are critical to understand.

- Tax-free qualified distributions from your account are not included in gross income if your account has been open for more than five years and you are at least 59½ years old or in the event of your death or disability, or if you qualify under the first-time homebuyer exception. A separate five-year holding period applies to each conversion transaction.

- Nonqualified distributions follow specific ordering rules. The distribution ordering rules require that all Roth IRA accounts be combined. The way the withdrawals are treated is as follows going up the following order:

- Contributions first: Where you have multiple Roth IRAs the initial amounts withdrawn represent your annual contributions. Because Roth contributions are not deductible, they are not subject to tax and can be taken at any time.

- Conversions second: Following the distribution of all contributions, any completed conversions represent the next distribution amounts. Conversion amounts from Roth IRAs follow a tax-free first-in, first-out distribution pattern. A 10% extra tax applies to converted funds taken before the five-year period expires or before reaching age 59½ unless a special exception exists. A separate five-year holding period applies to each conversion transaction.

- Gains last: The final distributions come exclusively from earnings.

The 10% additional tax does not apply to distributions for individuals who have reached age 59½ or in cases of death and disability. It also exempts distributions used for eligible medical expenses and health insurance premiums for specific unemployed individuals.

Roth IRA Withdrawal for non-US Expat in UK

Roth Individual Retirement Account payments to a UK resident that are not taxable in the United States are not taxable in the United Kingdom

Qualified distribution from Roth IRA

A qualified distribution from a Roth IRA is neither counted towards the recipient’s gross income nor does it attract the 10-percent additional tax for early withdrawals. The Roth IRA distribution must be delayed until after five years from the initial tax year in which the individual made a contribution to the Roth IRA for it to qualify as a “qualified distribution”. The five-year holding period concludes at the close of the fifth consecutive tax year from when the individual began the holding period.

The optimal conversion strategy from IRA to a Roth IRA

A traditional IRA conversion to a Roth IRA creates creates numerous possibilities for tax strategy and building wealth over time. Given the HMRC tax change in March 2025 of lump sum withdrawals, the value of Roth IRAs in pension planning has grown. The conversion strategy can be done in a partial amounts or the full US Pension with each method resulting in different tax outcomes and advantages. To ensure sound retirement planning decisions, you should learn about conversion processes and their federal income tax obligations.

To maximise tax benefits convert when your income drops and you will be a lower tax bracket. Should your yearly US income drop from $100,000 to $50,000 you can convert $30,000 from your traditional IRA for reduced tax rates. One practical approach is to convert enough funds from your retirement account to completely use up your existing tax bracket but remain below the threshold of the next tax bracket.

Tax-loss harvesting enables you to minimise conversion taxes by generating capital losses by selling depreciated investments to balance the extra income from the conversion.

When you convert only a portion of your funds, your taxable income increases by the amount converted. When you convert $25,000 from your traditional IRA into taxable income and your annual earnings are $75,000 your total taxable income is $100,000. The incremental approach enables taxpayers to manage their tax burden more effectively by distributing it over multiple years. The income from each partial conversion is subject to the tax rate that applies to your highest income bracket for that particular year. This technique gives you control over your tax burden and helps you steer clear of higher tax brackets, which would otherwise charge you rates of 32%, 35%, or even 37% on parts of your converted funds.

Retirees enjoy tax-free growth and withdrawal benefits with Roth IRA conversions. An individual with 20 or more years until retirement can see substantial benefits from tax-free compounding, which will outweigh the initial tax payment. The absence of required minimum distributions in Roth IRAs means your assets can grow indefinitely throughout your life. Beneficiaries receive tax-free inheritances from Roth IRAS, which makes them effective tools for estate planning. People expecting to fall into higher tax brackets during retirement or those who want to transfer tax-efficient assets to their heirs will find this approach very advantageous.

Full conversions streamline the procedure yet generate significant immediate tax obligations. Turning a $500,000 traditional IRA into a Roth IRA would increase your taxable income by the complete conversion amount and may result in placement into the top tax bracket. Partial conversions need additional planning but enable better tax management. By taking $50,000 each year from the $500,000 IRA across ten years, you will maintain lower tax brackets throughout this period. Your current tax situation, along with available funds for conversion taxes and long-term financial goals, determines the appropriate choice. Your age, together with your planned retirement date, plays a crucial role in this decision-making process.

Decisions between partial or complete conversion must be consistent with your overall financial plan. Roth conversions demand current tax payments but offer more substantial financial advantages over time. A financial adviser can help you create a conversion strategy that considers your present and expected tax brackets, your retirement schedule, and estate planning objectives. Through appropriate planning, IRA-to-Roth conversions boost both retirement security and legacy planning.

Paying tax for conversions from IRA / 401k to Roth IRA

When you finance Roth conversions using the converted funds to pay the taxes instead of external funds, you reduce the value of the converted funds because you are reducing the amount in the tax-advantaged account plus any incremental growth that sum could have generated. Choosing to finance Roth conversions through converted funds will require a calculation on how much should be withheld by the institution. If the withheld tax is not enough, taxpayers must pay a sufficient amount of “estimated tax”.

Pre-retirement Roth IRA conversions when the penalty is worthwhile

When you perform a Roth conversion, any taxes withheld are considered a taxable distribution, which could incur early withdrawal penalties if you are younger than 59½ and no early withdrawal rules apply. The penalty will apply to 10% of the amount of tax withheld (no 10% of the full converted sum). There may be situations where the 10% penalty is worth considering if you are in low-tax year and do not expect a similar opportunity in future years. The table below provides an example.

| Parameter | Value |

| Pre-tax balance converted | $20,000 |

| Current tax rate on conversion | 10% |

| Tax due on conversion (10% of $20,000) | $2,000 |

| Early‐withdrawal penalty rate | 10% |

| Amount subject to penalty | $2,000 |

| Penalty paid (10% of $2,000) | $200 |

| Total cost (tax + penalty) | $2,200 |

| Effective tax rate on conversion | 11% |

| Expected future marginal tax rate (retirement) | 22% |

Don’t pay income taxes from the conversion amount

You can pay the taxes due from my conversion of the retirement assets. While this is possible, it generally does not make sense to use the retirement assets to pay the taxes. If you are under age 59 1/2, the amount distributed to pay taxes may be subject to an IRS 10% additional tax for early or pre-59 1/2 distributions. It is recommended to use assets outside of retirement accounts to pay any taxes from the conversion, as this leaves the retirement funds to grow tax-free within the Roth IRA.

Where can I find more information on Roth conversions?

To learn if a Roth IRA can benefit you in your circumstances, speak to Edale. Our contact details and methods to speak to us are below.